A Painstaking Move for 30-Yr Interest Rates Ahead

Higher interest rates may be ahead still within the context of a secular bull market in bonds.

“Men, it has been well said, think in herds; it will be seen that they go mad in herds, while they only recover their senses slowly, and one by one.”

Extraordinary Popular Delusions and the Madness of Crowds – Charles Mackay

The discipline of security selection is part art and part science.

The science focuses on the sterile measurement and quantification of the concept of ‘value’.

The art is the assignment of a probability that a security moves to its assessed value.

As the CIO of Atlanta Capital Group I recognize that our investment committee members distill information differently and ply their trade based on subjective criteria that matches their own emotional makeup. AND THAT’S FINE.

So long as research is logically thought out and passes the common sense test my experience is that most disastrous investment decisions are avoided.

That means our culture focuses on decisions based on three schools of security analysis – Fundamental, Technical (I will call it Visual so as to avoid the emotional response it conjures) and lastly Sentimental.

For the purposes of this discussion – interest rates where to? – allow me to dwell on the last 2 disciplines and let us agree upfront that US Government bonds are richly valued given the historical low interest rate environment.

Crowd Sentiment

The most common refrain we have heard over the last 7-years (since the 2008 crisis) is – “Rates have nowhere to go but higher.”

We noticed a subtle shift in the mass psychology about a year ago where the common refrain became – “When rates eventually move higher” as exacerbated forecasters recognize that rates have stubbornly refused to move higher.

Then we noticed with interest this October 18th Bloomberg article – China’s Selling Tons of U.S. Debt. Americans Couldn’t Care Less.

China is beginning to disgorge of its $1.4 trillion U.S government bond horde but other buyers – US institutions, US retail and other Foreign entities – are soaking up the supply as well as all the new issuance in a now $12.9 trillion bond market!

It’s a convincing article with all the hallmarks of justifying bubble behavior to refute the higher interest rates argument:

Investors in the U.S. “are making a decision based on their outlook and it’s a reflection of the economy as well as their risk aversion,” Nomura’s Goncalves said.

[GS: is buying bonds at these levels an indication of risk aversion?]

Visual Analysis

The following chart shows an interesting floor exists on 30 Year T-Bond Rates.

Figure 1 – 30 Year US T-Bonds

The 2.5% level has acted as a floor 3 times now – in 2008 during the financial crisis, in 2012 during QE3 and early in 2015 during what will be called the Chinese growth implosion (rates moved temporarily below the floor only to bounce back swiftly).

Certainly from a visual perspective 2.5% is statistically meaningful.

Now we really have no idea whether we are entering a large secular bear market in bonds but we merely lob the question – what would be the effect of a sizeable correction in the bond market [albeit still within a bull market context] ?

We think we are about to find out over the next 12 months.

Figure 2 – 25 year price channel US T-Bonds

Since 1990 30-YR Bond prices have been moving in a well-defined channel (above) with regular oscillations between the top and bottom of the channel lines — all within the context of a secular bull market in Bonds.

Having hit the top of the channel in early 2015, it is feasible that prices can make their way to the bottom channel line as they had been doing for the preceding 25 years!

When could this happen?

It seems these periods of oscillation takes between 1 and 2 years so we would speculate 2016 / 2017.

Such a move from the peak to trough would indicate an approximate capital loss of 20% on 30-Yr Treasuries. At a current yield of 3% that is approximately a loss of 7 years’ worth of interest payments!

How would Pension funds deal with this loss? How would Risk-Parity strategies deal with this loss? Sovereign Wealth Funds, Insurance companies – how would most liability sensitive fixed income investors handle such a loss? Probably not well.

What would cause higher interest rates?

The exact reason is of course beyond our intellect but we could speculate:

- Fed hikes short term rates and the yield curve adjusts higher across all durations;

- Growth oscillation – the market has swung too far towards the deflationary side and adjusts in the opposite direction;

- Chinese selling finally overcomes the mass of buyers;

- The Fed starts to adjust its balance sheet with negative consequences (unlikely to happen);

- An exit for the door of a crowded trade;

Knock-on effects

Interest rate movements have consequences for all other asset classes Real Estate in particular.

Also, companies with a lot of newly issued investment grade debt may see deterioration in their credit ratings with a knock on effect on their equity prices.

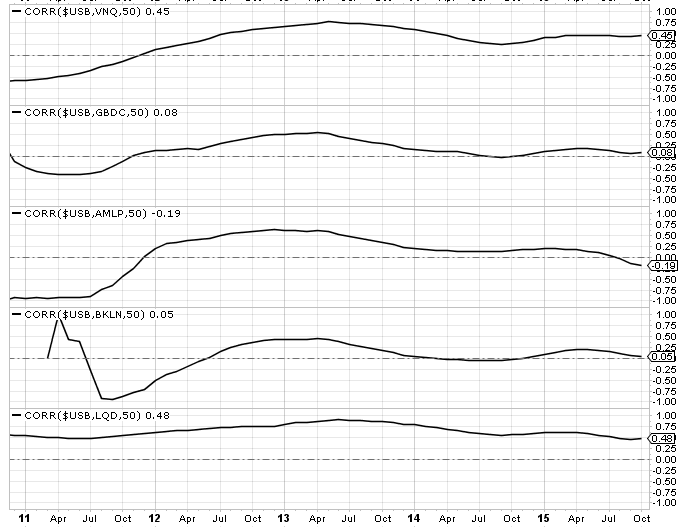

The following chart shows rolling correlations of Real Estate, BDCs, MLPs, Bank Loans and Investment Grade Credit (respectively) against the 30-Year Bond. Most are positively correlated meaning lower bond prices translate into lower prices.

Figure 3 – Rolling correlation Real Estate, BDCs, MLPs, Bank Loans, Investment Grade Bonds w US T-Bonds

What to Do to protect against higher interest rates?

We will stick with our decision to sit on a larger than normal cash allocation – despite the fact that it has no current yield – it may pay us very well when we come to buy assets at discounted prices!

— Greg

p.s. this is a great read for serious market students

—

Thank you for reading my post. Please sign up for our newsletter which contains private investment opportunities and other great information.

Nothing in this article should be interpreted as a recommendation to buy any security. Please consult your financial advisor & conduct your own due diligence.